Dmitry Vinogradov

Societe Generale believes the S&P 500 (SP500) is at a “critical juncture” and outlined two scenarios wherein Wall Street’s benchmark index could crater to 4,000 points or soar into ‘bubble’ territory above 6,600 points.

The S&P (SP500) has advanced more than 14% YTD, driven by a ferocious rally in technology stocks on the back of an ongoing craze around artificial intelligence (AI), and the expectation that the Federal Reserve will begin to cut rates if inflation data remains positive as it has been recently.

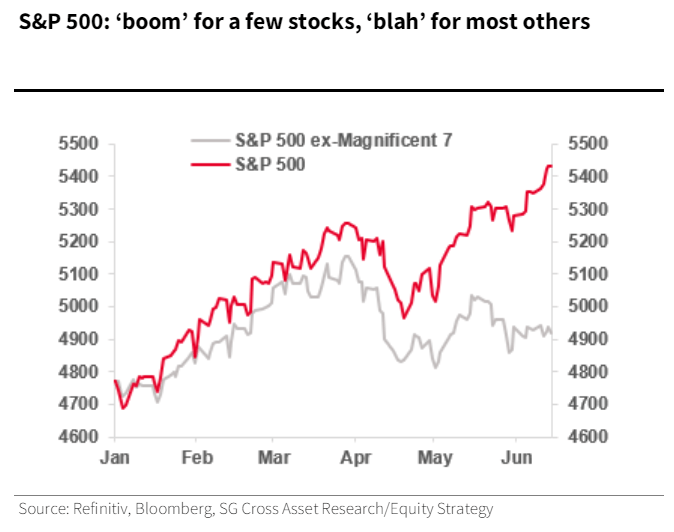

However, a simmering concern among investors amid this inexorable bull run has been market breadth – the S&P’s (SP500) 2024 gain has been largely due to a massive jump in the “Magnificent 7” club, with the average S&P stock struggling to keep up.

“Indeed, without the ‘Magnificent 7’ (Mag-7) stocks, the S&P would be up only 4%. Nvidia (NVDA) alone has gained 174% YTD; it is the index’s best performer and has the highest market cap, with the stock accounting for 40% of the S&P 500’s (SP500) total YTD gains,” Societe Generale’s Manish Kabra and Charles de Boissezon said in a research note on Monday.

“To illustrate this point, the Equal Weight S&P 500 (RSP) has gained just 4%, underperforming the U.S. benchmark by a wide margin,” they added.

The analysts believe the outperformance of the megacap technology stocks versus the average S&P stock is now at a “critical juncture.”

See below for a chart comparing the performance of the S&P 500 with and without the “Magnificent 7” club:

According to Societe Generale, such narrow market breadth typically occurs when there is either a bear market phenomenon typically seen in an economic recession, or when there are a concentrated number of high-performing names that have the potential to push markets into bubble territory.

“What if there is a recession? We don’t think investors will make a recession trade unless the Fed starts hiking again, which is by far not our base case. Yet, if small firms’ profits are hard hit and unemployment rates surpass >=5%, we could see the S&P 500 (SP500) dipping back to around the 4,000 mark – a low-probability event at this stage,” Kabra and de Boissezon said.

“What if there is a bubble? On the flip side, if the S&P 500 (SP500) accelerates further, with only a few stocks delivering a more significant re-rating than the others, and if the index trades at valuation levels similar to the peak reached in 1999-2000, we believe that the S&P 500 (SP500) could move to an upside scenario of 6,666 (24.7x in March 2000 x $270 2025e S&P 500 EPS),” the analysts added.

The brokerage kept its year-end target for Wall Street’s benchmark index unchanged at 5,500 points. The S&P (SP500) crossed that historic milestone last week on June 20, and closed out Tuesday’s trading session at 5,469.30.

“We like Tech and stay Overweight on it. However, as the profit cycle outside the Nasdaq-100 (NDX) companies should move from -10% in 2023 to +8% in 2024e, we have identified cyclical opportunities outside Tech too. So, instead of taking cyclical risk within Tech, where high-risk stocks have already performed well, we suggest opting for Financials and Industrials,” Societe Generale’s Kabra and de Boissezon said.